4 min read

Why ERPs Are the Next Fintech Platforms: The Rise of Embedded Payments in B2B SaaS

For years, Enterprise Resource Planning (ERP) software was the essential, if not exactly glamorous, engine of a business. It remains a back-office workhorse. It handles the books, manages inventory, and tracks projects. Essentially, it’s where the real work gets logged.

The problem, however, was that these systems have always been separate from how the money moves in practice. That was what your bank was for.

But that’s now changing, as ERPs undergo a structural transformation. The focus is shifting from logging tasks to actually completing them, and that means adding what was missing in the first place: the payments, physical and virtual cards, and the accounts.

The Financial Case for Adding Payments to ERPs

Obviously, the most compelling reason for this shift is the business model. It’s an opportunity to build a better product and, at the same time, increase earnings.

Until recently, all those fees around the software – like transaction commissions or card interchange – simply went straight to the banks. ERPs did the hard work of organising the business, but a third-party bank got paid when money had to move.

Now that separation is no longer necessary. What’s more, the financial upside of it is significant. A recent report from OC&Cspelled it out: B2B software platforms that embed financial features can see their earnings jump by 20-30% within a two-to-three-year period.

The report also goes on to detail exactly how this new, high-margin revenue is captured. Unsurprisingly, it comes from sources that were previously left for banks: interchange fees on card transactions, monthly subscription fees for premium financial features, and interest generated on funds deposited in accounts.

Finally, the “cost to play”—that is, the cost to the software provider—is estimated to be only around 30% of the new revenue generated. In other words, the majority of income from these new financial features can flow directly to the bottom line.

A Strategy Already in Practice

We’re not talking theory here. Several of Europe’s most prominent software players have already recognised the advantages of treating payments as a feature rather than a separate industry.

Take a look at Sage, the UK’s largest accounting software provider. They now deeply integrate payments, letting users send invoices with a “Pay Now” button that automatically reconciles. Visma, the Nordic software giant, integrates e-invoicing, payroll, and expense management. Xero and QuickBooks have captured their massive European user bases with the same model.

All of them now function as active financial hubs, not just passive and straightforward ledgers.

A Better Workflow, A “Stickier” Product

The model also works because it solves a core, and deeply inefficient, business process. Finance teams are often forced to work across several disconnected systems.

So, for instance, they might look up an invoice in the ERP, manually log in to their bank portal to schedule the payment, then return to the ERP to mark the same invoice as “paid.” That’s slow, manual, and error-prone.

But when financial features are embedded in the product, this entire manual loop disappears. Is the invoice in the system? You simply click “Pay.” Does the marketing team need a budget? You issue a virtual card with a specific amount limit, right from the project dashboard. The transaction is tracked, reconciled, and categorised immediately.

And then there is the customer retention aspect. When the platform becomes the single, indispensable tool for running the entire business, your product “sticks.” Why would a client ever leave?

The Old Barrier: “But We’re Not a Bank”

If the opportunity is so significant, why has this only just begun?

Historically, you had to be a bank to do it. There was simply no other way around it. The barriers to entry were colossal: acquiring banking licences, managing multi-million-euro compliance teams, building fraud engines, and negotiating partnerships with card schemes like Visa. For a software company, the cost, risk, and complexity were simply not worth it.

Today, you no longer need to be the bank. Instead, you can now partner with a licensed infrastructure provider that handles the complex parts.

The Infrastructure for the New ERP

To sum up, the model, known as “embedded finance,” splits the responsibilities. The enabler handles the financial license, compliance, and core payment infrastructure. The ERP platform, in turn, does what it does best: it owns the customer relationship and the user experience.

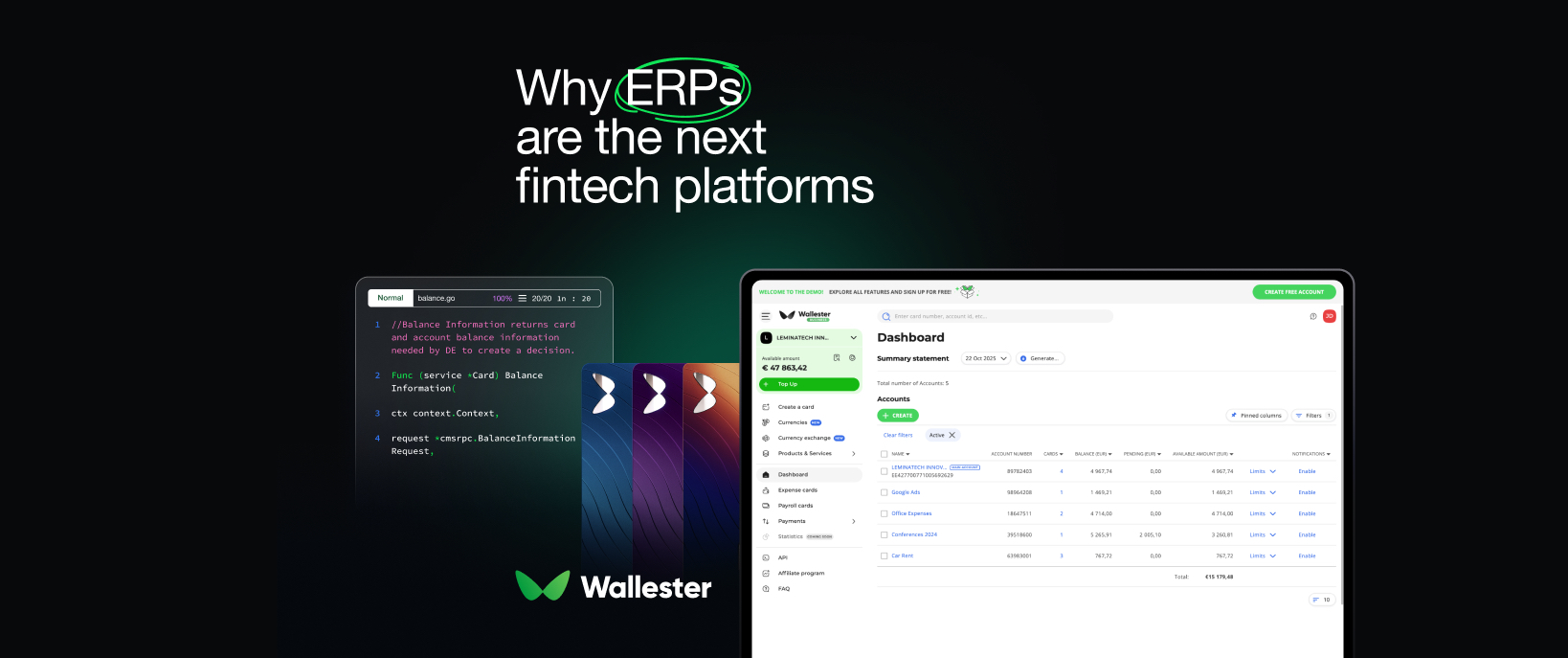

Wallester White-Label was designed to enable ERPs to do precisely that. We are the licensed, regulated engine running invisibly in the background, providing the financial rails through our API. This means an ERP provider can:

- Add financial features to the product in weeks and not months

- Issue branded virtual and physical Visa cards from their own platform

- Set granular spend controls for their clients – like custom limits or merchant allowlists – all managed within the single interface

- Handle multi-currency accounts and payments seamlessly

- Take on zero regulatory risk or compliance burden, as we handle it all

ERP systems are moving beyond bookkeeping into day-to-day financial management. Integrating payments and cards, instead of relying on external infrastructure, is the natural progression – and Wallester makes it straightforward to do.