4 min read

37% of the B2B Payment Cycle Is Delayed. Here’s What Finance Teams Can Actually Control

A recent study from Sidetrade, based on more than $ 8trillion in anonymised B2B transactions across 42 million buying companies, puts a number on something most finance teams already know: late payments are not a glitch but a structural issue.

Globally, 37% of the payment cycle now falls after the due date. The average business waits 51 days to get paid – 32 of those are contractual terms, and 19 are just pure delay. The gap is not shrinking, and regulation has not fixed it. For example, the EU outperforms the US on payment discipline (18 days of delay versus 29), but even within Europe, the variation is enormous. The Netherlands averages just 12 days of delay. Spain and parts of Southern and Eastern Europe lag by weeks, despite operating under similar legal frameworks.

In the US, a 25-day average delay masks significant industry-level differences. Financial services, insurance, and real estate average 57 days to pay, with 27 of those in delay. Manufacturing holds 24 days of delay, and it’s the same with HR services. In short, when you get paid obviously depends less on your contract terms and more on who you’re invoicing and where they sit.

The Incoming Side Is Largely Out of Your Hands

So this is worth saying plainly. You can, of course, chase invoices harder, tighten credit terms, or segment risk more aggressively. And you should. But it’s difficult to force a client in financial services to pay like a manufacturer or transform Southern Europe into the Netherlands. More importantly, it’s difficult to budget on the assumption that contractual terms mean anything when nearly four in ten payment days fall outside them.

If 37% of your incoming cash is structurally hard to predict, planning around it might be a losing game. You can improve it at the margins, but you cannot really control it.

So What Can You Control?

What goes out.

Most finance teams spend disproportionate energy on the receivables side, including chasing, forecasting, and modelling. At the same time, the payables and expense side runs on loose approvals, monthly reconciliations, and a general hope that nothing too expensive slips through.

But that’s the wrong balance. When your incoming cash is unreliable, the single most important thing you can do is make your outgoing spend predictable, visible, and adjustable. That means knowing – in real time, not at month-end – who is spending what, on which categories, and whether it aligns with what was planned.

Three Things That Can Help

First, real-time visibility. If your expense data comes in batches – weekly reports, monthly reconciliations, quarterly reviews – you are always reacting to what already happened. You need a live picture of what is going out, updated as transactions happen, not when someone gets around to filing a report.

Second, pre-set controls. Approval workflows and spending limits that exist before the money leaves, not after. This is not about micromanaging every purchase. Setting boundaries that match your current cash position is of strategic importance. When a slow month hits on the receivables side, the damage on the payables side is already contained.

Third, flexibility. Fixed annual budgets assume stable income, which, as the Sidetrade data makes clear, most businesses do not have. You need the ability to adjust limits and categories quickly – tightening in lean months, loosening in strong ones – without rebuilding the entire system each time.

A Simpler Way to Control What Goes Out

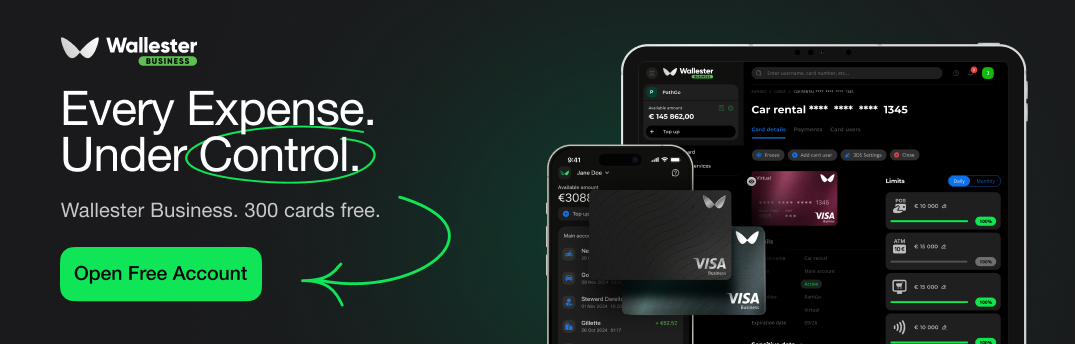

Wallester Business was designed for finance teams that need clarity and control over company spend. It’s a financial operating system that helps you manage outgoing expenses – whether that’s across departments, categories, or teams.

One of its most practical features is real-time spend tracking. Every transaction is visible the moment it happens, not when someone submits a receipt. The budget picture is always current, which matters most when incoming cash is unpredictable.

And beyond real-time visibility, Wallester Business also gives you:

- 300 free virtual Visa cards – unlimited users, no time limits

- Pre-set spending limits – by card, employee, or category

- Unified dashboard – track and control all spend from one place

- Tokenised cards – works with Apple Pay, Google Pay, Garmin, and more

- Payroll & team cards – up to 1,500 transactions in one click

- Native integrations with Xero and QuickBooks + REST API – connect to your internal systems and automate accounting

It will not fix delays on incoming payments. Most likely nothing will, short of structural change in how entire industries pay their suppliers. But it gives you full control over the other side of the equation – and when cash is tight, that is the side that matters most.