New data from the Global Payments Report 2026 puts hard numbers behind a shift most people in payments have been sensing for a while, and that’s the steady rise of digital wallets.

Yes, cards are still holding their ground. For example, in 2025, 49% of US online shopping and 71% of in-store spending was done via credit or debit cards. However, digital wallets are steadily eating into that share. By 2030, direct card use is forecast to fall to 42% in e-commerce and 61% in-store.

What about Europe? Digital wallets account for 18% of point-of-sale value today. That is below the global average of 33%, mainly because the card infrastructure here is already good. But the forecast is for 12% compound annual growth through 2030, pushed along by the opening of Apple’s NFC function to non-Apple providers and the arrival of Wero, a regional wallet built specifically for the European market.

In any case, the direction is the same. In short, digital wallets are becoming the default for a growing share of everyday spending.

Why It Makes Sense

The case for digital wallets is straightforward. No more searching your pockets or doing strange choreography with your wallet. You tap your phone or watch, the payment clears, and you move on. For anyone who travels regularly, works across locations, or just wants fewer things in their pockets, it is simply a better experience.

Security is part of it too. Tokenisation means your actual card details are never shared at the point of sale. The wallet generates a one-time code for each transaction instead. In that sense, it is more secure than a physical card, even a chip-and-pin one.

Then there is the generational angle. For Gen Z, digital wallets and tap-to-pay are already the norm, and as their spending power grows, their payment habits are a reasonable indicator of where things are heading.

The Same People Work Somewhere

That’s the consumer story, and the corporate one follows from it. The people who default to a digital wallet when buying groceries do not suddenly change their expectations when they sit down at an office desk. If pulling out a physical card already feels like unnecessary friction in personal life, it will feel the same when managing work expenses the old way – carrying a card, submitting receipts, or waiting for reimbursements.

“Clients with remote or travelling teams now treat Apple Pay and Google Pay as essential. Today, if staff have to wait for a physical card before they can spend, it is seen as a delay. We are hearing this from businesses of all sizes and sectors,” says Mattia Piazzano, client relationship manager team lead at Wallester

The practical case for corporate digital wallet integrations is much the same as the consumer one. Tap-to-pay is faster, and card details are not exposed. For employees who travel, not having to carry a physical card is simply more convenient. And for finance teams, it makes life easier as well, because the spend is tracked, limits can be applied, and the dashboard shows whatever needs to be shown.

“The real shift is in how spend moves. Transactions flow in real time, records stay accurate, and finance teams get visibility from the first purchase rather than at month-end reconciliation. And employees love it too. They add the card to their phone and it becomes how they pay from day one,” Piazzano adds.

“Companies are no longer debating whether to support digital wallets. That is the new standard. The question now is how to roll it out to the entire team at once. If you are issuing cards today, employees assume they will work with their phones,” he says.

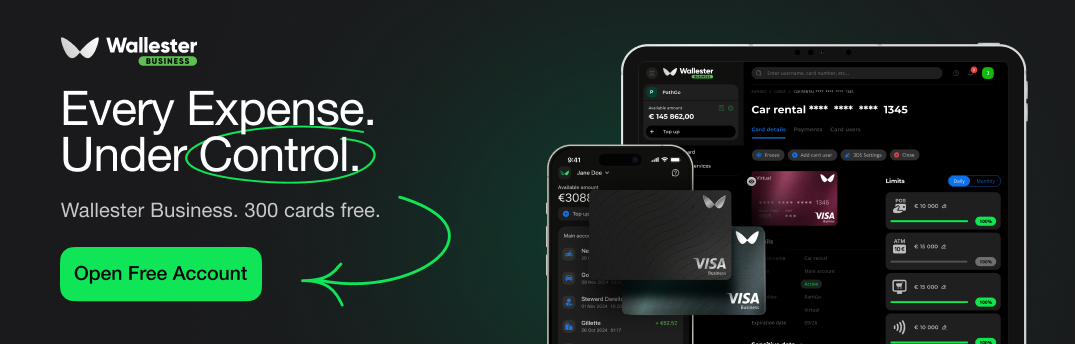

What this really comes down to is demographics. A generation that expects payments to be phone-first is entering the workforce in growing numbers, and corporate card setups will have to keep pace. If your team is already paying by phone in their personal lives, here’s what Wallester Business gives you:

- Digital wallet compatibility – Add your corporate card to Apple Pay, Google Pay, or Garmin Pay instantly. No extra setup, no waiting for a physical card.

- 300 free virtual Visa cards – One per department, vendor, or subscription. Every card named, budgeted, and tracked independently.

- Pre-set spending limits – Hard limits by card, employee, or category. Set before the spend happens, not after.

- Unified real-time dashboard – Every transaction visible the moment it is authorised, not at month-end.

- Payroll and team payments – Up to 1,500 transactions in a single click.

- Native integrations – Direct sync with Xero and QuickBooks, or custom flows via REST API.